In the complex landscape of Goods and Services Tax (GST) compliance, few areas demand as much attention as the issuance of tax invoices. For businesses engaged in providing continuous services spanning months or years, the timing of these invoices is governed by specific provisions under Section 31(5) of the Central Goods and Services Tax (CGST) Act, 2017. This provision contains three distinct sub-clauses that outline different scenarios for invoice issuance, raising important questions about their application: Do service providers have the freedom to choose which sub-clause to apply? Or are these provisions mutually exclusive and determined by contractual terms?

This article examines these questions and provides clarity on the correct application of Section 31(5) for continuous supply of services.

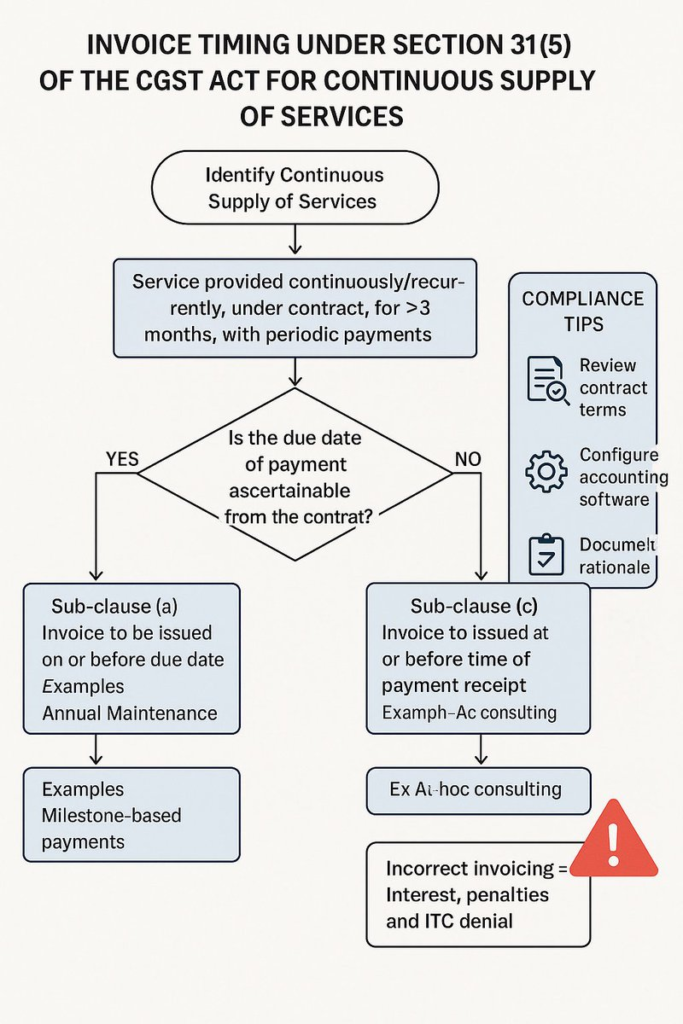

What Constitutes a “Continuous Supply of Services”?

Before delving into invoice timing requirements, it’s essential to understand what qualifies as a “continuous supply of services” under GST law. Section 2(33) of the CGST Act defines this as a service that is:

- Provided continuously or on a recurrent basis

- Under a contract

- For a period exceeding three months

- With periodic payment obligations

Typical examples include Annual Maintenance Contracts (AMCs), long-term software support agreements, rental arrangements extending beyond three months, and telecommunication services.

The Three Sub-clauses of Section 31(5): Understanding Their Distinct Applicability

Section 31(5) provides three different scenarios for determining when to issue a tax invoice for continuous services:

Sub-clause (a): When Due Date is Ascertainable from Contract

The first scenario applies when the contract clearly specifies payment due dates. The provision states: “where the due date of payment is ascertainable from the contract, the invoice shall be issued on or before the due date of payment.”

For example, in a 12-month software maintenance contract with quarterly payments due on the 1st of April, July, October, and January, invoices must be issued on or before these specified dates.

Sub-clause (b): When Due Date is Not Ascertainable from Contract

The second scenario applies when the contract does not specify clear payment due dates. In such cases, “where the due date of payment is not ascertainable from the contract, the invoice shall be issued before or at the time when the supplier of service receives the payment.”

For instance, if a consulting agreement stipulates that payments will be made “based on fund availability” without fixed dates, the consultant must issue invoices before or when they receive payment.

Sub-clause (c): When Payment is Linked to Event Completion

The third scenario applies when payment depends on completing specific events: “where the payment is linked to the completion of an event, the invoice shall be issued on or before the date of completion of that event.”

An example would be a software development contract where 30% payment is due upon completion of “Phase 1: User Interface Design.” The invoice for this portion must be issued on or before the date Phase 1 is completed.

No Arbitrary Choice: Contractual Terms Determine Applicable Sub-clause

A critical question is whether service providers can arbitrarily choose which sub-clause to apply. The analysis of Section 31(5)’s structure and language reveals the answer is no.

Each sub-clause begins with the conditional term “where,” indicating that each provision is designed to apply to a specific and distinct factual scenario defined by the contract’s payment terms. This linguistic structure strongly suggests mutual exclusivity among the sub-clauses.

The conditions within each sub-clause—an ascertainable payment due date, a non-ascertainable due date, or payment linked to event completion—are inherently different. It’s difficult to conceive how a single payment obligation could simultaneously satisfy the distinct conditions of multiple sub-clauses.

Official circulars support this interpretation. For example, CBIC Circular No. 222/16/2024-GST addressing spectrum usage charges treats the Frequency Assignment Letter as a contract. The circular explicitly states that if this document specifies ascertainable payment due dates, Section 31(5)(a) mandatorily applies.

Therefore, the applicable sub-clause is determined by the objective contractual terms agreed between supplier and recipient, not by the service provider’s preference.

A Logical Assessment Process for Determining the Applicable Sub-clause

While Section 31(5) doesn’t explicitly establish a formal hierarchy among its sub-clauses, a logical sequence for their assessment emerges:

- First, check whether the due date of payment is ascertainable from the contract. If yes, apply sub-clause (a).

- If not, determine whether payment is linked to the completion of a specific event. If yes, apply sub-clause (c).

- If neither of these conditions applies, default to sub-clause (b).

This structured approach ensures systematic coverage of all contractual payment possibilities.

Can Multiple Sub-clauses Apply to a Single Invoice?

Given the principle of mutual exclusivity, it’s highly improbable for more than one sub-clause to apply simultaneously to the same component of service covered by a single tax invoice.

However, a complex contract might involve different types of charges that, if invoiced separately, could legitimately fall under different sub-clauses. For example:

- A fixed monthly retainer (Section 31(5)(a))

- A performance bonus upon project phase completion (Section 31(5)(c))

- Ad-hoc charges for additional services without fixed payment dates (Section 31(5)(b))

In such scenarios, different invoices would be issued for different service components, each following its relevant sub-clause. But for a single invoicing event covering a specific supply portion, only one sub-clause can apply.

Practical Implementation and Compliance Steps

To ensure compliance with Section 31(5), service providers should follow these steps:

- Confirm “Continuous Supply” Status: Verify that the service meets all criteria under Section 2(33).

- Thoroughly Examine the Contract: Review payment terms to determine which sub-clause applies:

- Are payment due dates clearly ascertainable? → Apply sub-clause (a)

- Are payments linked to specific event completions? → Apply sub-clause (c)

- If neither condition applies → Apply sub-clause (b)

- Document Your Rationale: Maintain internal records explaining why a particular sub-clause was applied, supported by relevant contract clauses.

- Configure Accounting Systems: Ensure invoicing systems are set up to generate tax invoices according to the applicable timelines.

- Handle Advance Payments Separately: Remember that receipt vouchers must be issued for any advance payments, independent of the tax invoice requirements under Section 31(5).

Consequences of Non-Compliance

Incorrect application of Section 31(5) can lead to several adverse outcomes:

- Interest Liability: Delays in GST payment resulting from incorrect invoice timing can trigger interest charges (typically 18% per annum).

- Penalties: Non-compliance may attract penalties under various provisions:

- General penalty up to ₹25,000 under Section 125

- Penalties for incorrect invoicing or non-issuance of invoices

- Impact on Recipient’s Input Tax Credit (ITC): Perhaps most significantly, incorrectly issued or delayed invoices can jeopardize the recipient’s ability to claim ITC, potentially straining business relationships.

- Increased Scrutiny: Persistent non-compliance may flag a business for departmental audits.

Why This Matters: Strategic Implications

The correct application of Section 31(5) carries significant strategic implications:

- Contract Drafting Considerations: When negotiating continuous service agreements, parties should carefully consider how payment terms are structured, as this directly determines applicable invoicing timelines.

- Cash Flow Impact: The timing of invoice issuance affects when GST liability arises and must be discharged, impacting cash flow planning.

- Business Relationship Management: Ensuring timely and compliant invoicing facilitates smooth ITC claims for recipients, strengthening business relationships.

- Risk Management: Proactive compliance minimizes the risk of penalties, interest, and disputes.

Conclusion

Section 31(5) of the CGST Act provides a structured framework for invoice timing in continuous service arrangements. The analysis leads to several key conclusions:

- Service providers do not have arbitrary choice among sub-clauses (a), (b), and (c).

- These sub-clauses are mutually exclusive, each addressing a distinct scenario based on contractual payment terms.

- The contract is determinative—specific terms regarding payment due dates or event linkages dictate which sub-clause applies.

- It’s not permissible to apply multiple sub-clauses to a single invoice for a specific supply component.

For businesses engaged in continuous services, implementing robust processes for contract review and invoice timing is essential. This includes thorough contract analysis, clear documentation of applicable provisions, appropriate system configuration, and regular monitoring of regulatory developments.

By embedding these compliance practices into contract management and operational processes, businesses can achieve more than mere technical adherence to GST provisions—they can create strategic advantage through enhanced financial planning, reduced risk exposure, and stronger client relationships.

The complexity of Section 31(5) reflects the diverse commercial arrangements that characterize continuous service supplies. However, with systematic analysis and structured implementation, businesses can navigate these requirements effectively while optimizing their invoicing practices within the legal framework.