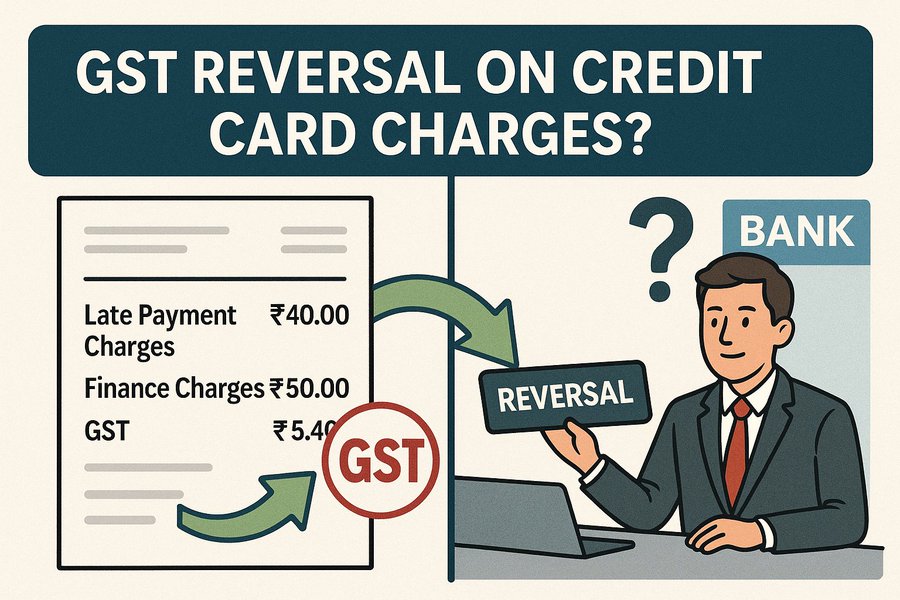

Short Answer: Yes!

The implementation of the Goods and Services Tax (GST) in India from July 1, 2017, marked a significant transformation of the country’s indirect tax structure. Banking and financial services, given their complexity and diverse offerings, presented unique challenges within this framework. A recurring point of contention arises when banks reverse charges such as late payment fees or finance charges along with the applicable GST. This analysis explores the legal obligations surrounding GST reversal when banks reverse underlying charges, focusing on the procedures mandated under the Central Goods and Services Tax Act, 2017 (CGST Act).

GST Applicability on Bank Charges

Legal Basis for Taxation

The foundation for levying GST on bank charges stems from the definition of ‘value of supply’ under the CGST Act. Section 15(2)(d) explicitly states that the value of supply includes “interest or late fee or penalty for delayed payment of any consideration for any supply.” When a bank provides a service, additional amounts charged due to the customer’s delay in fulfilling payment obligations are considered part of the value of the underlying banking service and are brought within the scope of GST levy.

Financial services predominantly fall under Service Accounting Code (SAC) 9971. Most ancillary banking services that involve explicit fees attract GST at the standard rate of 18% (levied as 9% CGST + 9% SGST for intra-state supplies or 18% IGST for inter-state supplies). This includes late payment charges, finance charges on credit cards, processing fees, annual fees, and similar levies.

Distinguishing Taxable Charges from Exempt Interest

It’s crucial to differentiate between taxable charges and exempt interest components. Notification No. 12/2017-Central Tax (Rate), dated June 28, 2017, provides an exemption for “services by way of extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount.” This exemption covers interest earned by banks on standard loans and advances and interest paid on deposits.

However, this exemption explicitly excludes “interest involved in credit card services.” This exclusion confirms that interest charged on outstanding credit card balances, often referred to as finance charges, is liable to GST at 18%. Furthermore, official FAQs clarify that any additional interest or penal interest charged for default in payment of installments related to a supply which is itself subject to GST, is includible in the value of that supply and hence liable to GST.

The Emergence of ‘Penal Charges’

A significant development occurred following a directive from the Reserve Bank of India (RBI) issued in August 2023. This directive mandated Regulated Entities (REs), including banks, to replace ‘penal interest’ with ‘penal charges’ for non-compliance with material loan terms and conditions. These penal charges are to be levied reasonably and non-discriminatorily on the defaulted amount only and should not be capitalized.

Subsequently, the Central Board of Indirect Taxes and Customs (CBIC) issued Circular No. 245/02/2025-GST, dated January 28, 2025, clarifying that these specific ‘penal charges’ are not subject to GST. The rationale provided is that such charges are akin to damages or penalties for breach of contract terms, rather than constituting consideration for a supply of service.

This creates a critical distinction in GST treatment based on the nature and timing of the charge:

- ‘Late payment fees’, ‘finance charges’ (especially on credit cards), and ‘penal interest’ levied prior to the RBI directive’s implementation generally remain taxable under Section 15(2)(d).

- ‘Penal charges’ levied strictly in accordance with the RBI’s August 2023 guidelines are exempt from GST.

GST Adjustment Mechanism for Reversed Charges

Credit Notes Under Section 34, CGST Act

When a bank reverses a previously levied taxable charge, this action effectively constitutes a reduction in the value of the service originally supplied. The CGST Act provides a specific legal instrument to handle such situations: Credit Notes, as defined under Section 34.

Section 34(1) outlines the circumstances requiring a registered person to issue credit notes:

- When the taxable value charged exceeds the actual taxable value payable

- When the tax charged exceeds the actual tax payable

- When goods supplied are returned

- When goods or services supplied are found deficient

The reversal of a taxable bank charge clearly falls under conditions (1) and (2). If a late payment fee was charged and later waived, the taxable value and tax originally charged exceed the final amount payable, statutorily triggering the requirement for the bank to issue a credit note under Section 34(1).

Procedural Requirements and Timelines

The bank must declare credit note details in their GST return (Form GSTR-1) for the month of issuance. There is a statutory time limit for declaring these credit notes for adjusting tax liability – no later than the 30th day of November following the end of the financial year in which the original supply was made, or the date of furnishing the relevant annual return (Form GSTR-9), whichever is earlier.

Rule 53(1A) of the CGST Rules, 2017 prescribes the specific particulars that must be contained in a credit note, including supplier and recipient details, unique serial number, date of issue, reference to the corresponding original tax invoice(s), value of supply, rate of tax, and the amount of tax credited.

No tax without transaction

Some banks may assert that “the GST component once charged will not be reversed” despite reversing the associated service fees is contrary to established GST law and is legally untenable. As per Section 34(1) of the CGST Act, 2017, the issuance of a credit note is mandatory when the taxable value of a supply decreases. The use of the word “shall” indicates a statutory obligation, not discretion.

Retaining the GST component after reversing the service charge amounts to collecting tax without an underlying supply, violating the fundamental principle of “no tax without transaction.” It either results in wrongful retention of funds belonging to the government or to the customer and creates inconsistencies in tax accounting.

Under Section 9 of the CGST Act, banks(or any other service provider) act merely as a conduit for tax collection and not as a beneficiary. GST collected on a reversed transaction is not banks revenue. Retaining it amounts to unjust enrichment, and may be in violation of Section 171.

Bnaks position also exposes banks to regulatory risk, including penalties under Section 122 for incorrect invoicing, interest under Section 50 for excess tax collection, and even prosecution under Section 132. Additionally, banks may be subject to consumer claims for systematic overcharging and unfair trade practices.

Further, CBIC Circular No. 137/07/2020-GST makes it clear that changes in consideration must be accompanied by corresponding tax adjustments. Although the circular addresses construction services, the principle applies broadly to all taxable services.

Banks are also legally obligated to issue a proper credit note detailing the original invoice reference, the decreased taxable value, the corresponding tax amount (CGST, SGST/UTGST, or IGST), and the reason—specifically, “Reversal of service charges.”

The Critical Link: Recipient’s Input Tax Credit (ITC) Reversal

A pivotal change was recommended by the 55th GST Council meeting in December 2024 and subsequently proposed for legislative amendment. This amendment to Section 34(2) introduces a critical condition for the supplier’s reduction of output tax liability.

The new requirement stipulates that a supplier (bank) issuing a credit note can reduce their output tax liability only if the recipient of the supply (the customer) has reversed the Input Tax Credit (ITC) that corresponds to the reduction in value specified in the credit note.

The objective of this amendment is to plug a potential revenue leakage loophole. Previously, a supplier could issue a credit note and reduce their tax liability, while the recipient might fail to reverse the corresponding ITC they had claimed based on the original invoice.

This amendment significantly alters the operational dynamics and compliance burden. It places the onus on the bank not only to issue the credit note but also to ensure that the recipient has performed the corresponding ITC reversal before the bank can legitimately reduce its own tax payment. Obtaining such confirmation presents a considerable operational challenge, which may explain banks’ reluctance or delay in reversing the GST component of charges.

Practical Scenarios

Scenario 1: Late Payment Fee Reversed (B2B)

When a business customer (registered under GST) is charged a late payment fee plus GST on their corporate credit card and subsequently gets it reversed:

Bank’s Action:

- Reverse the base charge

- Issue a GST Credit Note for the taxable value reduction and tax reduction

- Inform the business customer about their obligation to reverse the ITC previously claimed

- Obtain confirmation from the business that they have reversed the ITC

- Declare the Credit Note details in the bank’s GSTR-1

- Only after receiving confirmation of ITC reversal, reduce its output tax liability

Customer’s Action:

- Receive the Credit Note

- Reverse the ITC claimed earlier in their GSTR-3B

- Confirm the reversal to the bank

Scenario 2: Finance Charge Reversed (B2C)

When an individual (unregistered customer) is charged finance charges plus GST on their personal credit card and gets it reversed:

Bank’s Action:

- Reverse the base charge

- Issue a financial credit note documenting the reversal of the charge plus GST

- Declare the details of this reduction in their GSTR-1

- Reduce its output tax liability in its GSTR-3B

Customer’s Action:

- The customer, being unregistered, cannot claim ITC. Therefore, the requirement for ITC reversal does not apply

- The customer simply benefits from the total reversal

Impact of Amended Section 34(2) on Compliance

The requirement for banks to ensure recipient ITC reversal before adjusting their own liability presents significant practical hurdles:

- Communication & Coordination: Banks need robust systems to communicate the issuance of credit notes and the recipient’s obligation to reverse ITC.

- Verification: Establishing a reliable mechanism to verify that the recipient has actually reversed the ITC is difficult. Relying solely on customer confirmation might be risky from an audit perspective.

- Timelines: Delays in recipient confirmation could push the bank beyond the November 30th deadline for adjusting its tax liability, leading to a permanent loss of the tax amount for the bank.

- Disputes: If a customer disputes the need to reverse ITC or fails to do so, the bank is caught in the middle, unable to reduce its liability despite having reversed the charge.

This increased compliance burden might lead banks to be more cautious or slower in processing GST reversals accompanying charge reversals, potentially explaining observed delays in the system.

Official Clarifications and Jurisprudence

While specific circulars addressing the reversal of general bank charges seem scarce, the foundational principles are well-established:

- Taxability of Charges: FAQs and rate notifications confirm the taxability of late fees and credit card interest under SAC 9971 at 18%.

- Credit Note Mechanism: Section 34 and associated rules provide the general framework, with the recent amendment tightening the link to recipient ITC reversal.

- Penal Charges Exemption: Circular No. 245/02/2025-GST clarifies the exemption for specific penal charges mandated by RBI, distinguishing them from taxable late fees/interest.

Advance Rulings consistently uphold the taxability of ancillary bank charges. For instance:

- Re: Bajaj Finance Ltd. (Maharashtra AAR): Confirmed GST applicability on various penal and additional interest charges levied on customers for delayed EMI payments.

- Re: Cholamandalam Investment and Finance Company Ltd. (Tamil Nadu AAR): Held that additional/penal interest on delayed loan installments is part of the value of supply and taxable.

Conclusion

When banks reverse late payment charges or finance charges that were originally subject to GST, they are legally obligated under Section 34 of the CGST Act to also reverse the GST component collected on those charges by issuing a GST Credit Note to the customer.

However, the bank’s ability to reduce its own tax payment to the government based on this credit note is now contingent upon the registered customer reversing the corresponding Input Tax Credit. This recent amendment introduces a procedural complexity that may cause delays or require active participation from the customer (in B2B cases). For unregistered (B2C) customers, the bank can directly adjust its liability after issuing the credit note and reporting it.

Despite practical difficulties, the legal obligation under Section 34 remains. Any systemic refusal by banks to reverse GST alongside the base charge would likely be contrary to Section 34 and potentially challengeable. The operational difficulty introduced by the amended Section 34(2) may explain practical delays but does not extinguish the fundamental legal obligation.

Recommendations

For Banks:

- Implement clear internal procedures for issuing GST Credit Notes whenever taxable charges are reversed

- Develop robust communication channels to inform B2B customers about issued Credit Notes

- Explore mechanisms to obtain confirmation of ITC reversal

- Ensure timely reporting of Credit Notes in GSTR-1

- Clearly differentiate between taxable charges and exempt charges

For Customers (Businesses):

- Be aware that if a bank reverses a charge on which you claimed ITC, you are obligated to reverse that ITC

- Expect to receive a GST Credit Note for reversed taxable charges

- Cooperate with the bank by confirming ITC reversal promptly

- Escalate matters if a bank refuses to issue a GST Credit Note for the tax component

For Policymakers (GST Council/CBIC):

- Consider issuing further clarifications addressing the operational challenges arising from the amended Section 34(2)

- Enhance GSTN portal functionalities to facilitate easier matching and confirmation of credit notes and corresponding ITC reversals

References

- Central Goods and Services Tax Act, 2017, Section 15.

- Notification No. 12/2017-Central Tax (Rate), dated June 28, 2017.

- CBIC, “FAQ on Banking, Insurance and Stock Brokers Sector.”

- ClearTax, “GST on Banking Sector: Impact & Important Provisions.”

- BankBazaar, “GST on banking and financial services: Applicability, rates and more.”

- Masters India, “Impact of GST on Banking Sector.”

- Notification No. 11/2017-Central Tax (Rate), dated June 28, 2017.

- Bajaj Finserv Markets, “GST on Credit Card Transactions: Fees, Charges, Benefits, and More.”

- CBIC, “FAQ on Financial Services Sector.”

- SAG Infotech, “GST On Banking Services: Latest News and Impact.”

- Financial Express, “GST impact on banking services: Here’s the list of transactions to become costlier from July 1,” June 2017.

- RBI Circular: DOR.STR.REC.50/21.04.048/2023-24, dated August 18, 2023 – Fair Lending Practice – Penal Charges in Loan Accounts.

- CBIC Circular No. 245/02/2025-GST, dated January 28, 2025.

- Press Release: Recommendations of 55th GST Council Meeting, dated December 21, 2024.

- Business Standard, “GST Council decides penal charges by banks won’t attract GST,” Dec 2024/Jan 2025.

- CBIC Circular No. 178/10/2022-GST, dated August 3, 2022.

- ICICI Bank, “GST on Loan: Processing Fee, Interest Rates, EMI.”

- Central Goods and Services Tax Act, 2017, Section 34.

- TaxGuru, “Credit Note & Debit Note under GST – Section 34.”

- Central Goods and Services Tax Rules, 2017, Rule 53.

- Finance Act, 2022 amendments to Section 34, CGST Act.

- GST AAR Maharashtra, In Re: Bajaj Finance Ltd., Order No. GST-ARA-23/2018-19/B-69, dated July 26, 2018.

- GST AAR Tamil Nadu, In Re: Cholamandalam Investment and Finance Company Ltd., Order No. 12/AAR/2019, dated June 28, 2019.